The housing affordability crisis in the United States has reached alarming levels, making homeownership an elusive dream for many Americans. Spiraling costs have resulted from a combination of factors, including restrictive land-use regulations and NIMBY policies that stifle construction productivity. As prices for new homes have more than doubled since 1960, the housing market trends reflect a troubling landscape where many young families and first-time buyers face insurmountable homeownership challenges. The implications of this affordability crisis extend beyond individual struggles, affecting the overall economy and limiting innovative solutions in the real estate sector. Addressing these issues requires a multifaceted approach that tackles regulatory barriers and promotes sustainable development practices to restore balance in the housing market.

The ongoing challenge of housing affordability has emerged as a pressing issue across American communities, commonly referred to as the housing crisis. Various socioeconomic factors, coupled with stringent land-use laws and community opposition to new developments, have exacerbated the struggle for many to achieve stable living conditions. These bureaucratic obstacles not only hinder new construction but also diminish overall industry productivity, leading to a disconnect in housing supply. The rising prices have consequently created significant hurdles for prospective homeowners, particularly among younger generations. By examining innovative strategies and policies, stakeholders aim to reverse these troubling trends and make housing more accessible.

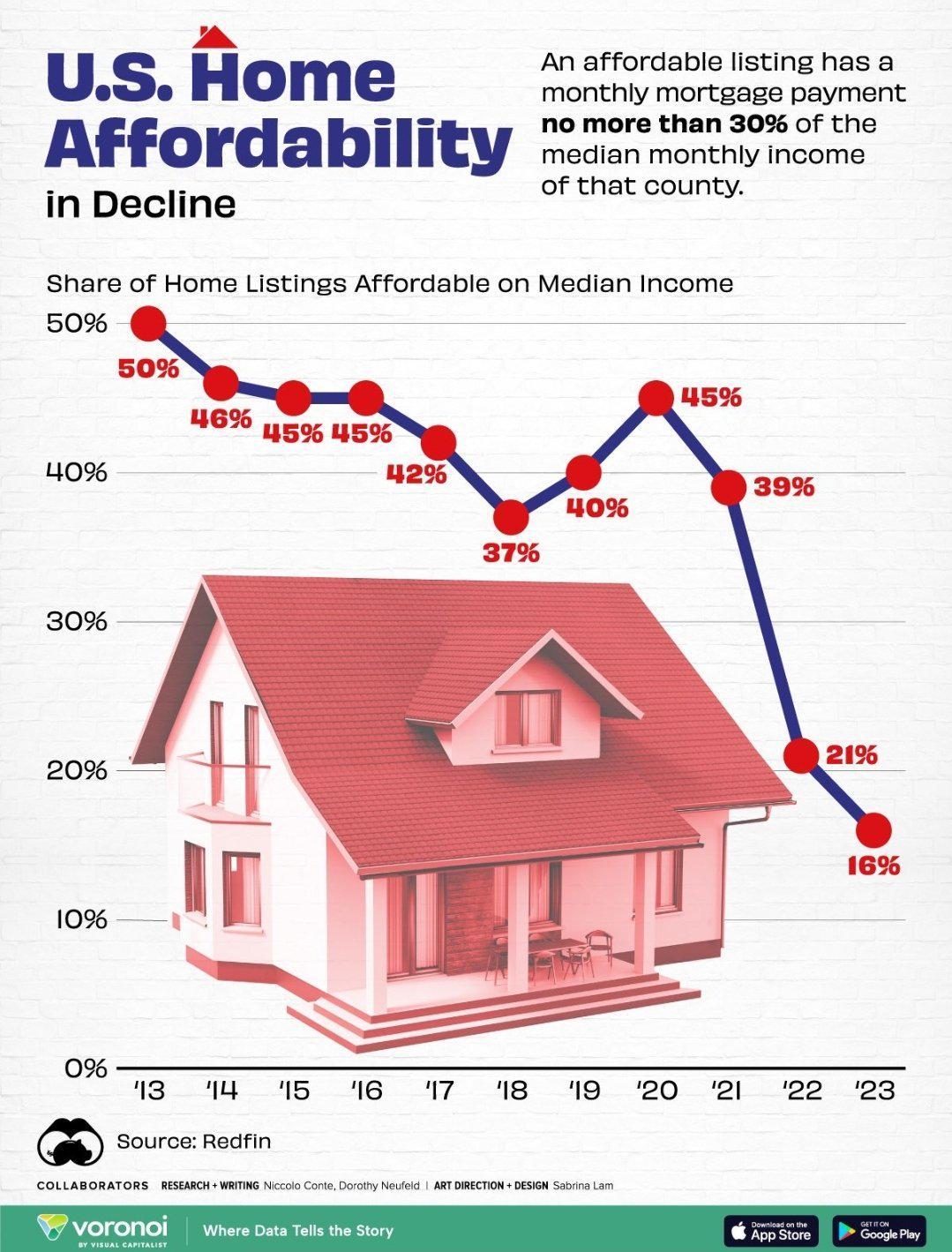

Understanding the Housing Affordability Crisis

The housing affordability crisis in the United States is marked by increasing home prices and stagnant wages, which place homeownership out of reach for many Americans. Recent research highlights that the average price of a single-family home has more than doubled since 1960, driven by a combination of rising labor and material costs. However, the stifling impact of land-use regulations and NIMBY policies has exacerbated this situation, reinforcing barriers that prevent adequate housing supply from meeting demand.

Many potential homeowners are facing challenges due to the soaring costs associated with homeownership, making it difficult for younger generations and low-income families to purchase homes. As the market is constrained by restrictive zoning laws and community opposition to new developments — often encapsulated by NIMBY sentiments — opportunities for affordable housing become increasingly limited, further contributing to the affordability crisis.

The Impact of Land-Use Regulations on Housing

Land-use regulations which dictate how land can be developed are a double-edged sword; while they aim to protect communities, they also serve as catalysts for the housing affordability crisis. Increased regulations and oversight have resulted in a significant decrease in construction productivity, leading to fewer new homes being built. These restrictions often require developers to meet multiple community demands, resulting in smaller, less efficient development projects that inhibit mass production strategies that once characterized the housing market.

Moreover, studies reveal that as land-use regulations have proliferated since the 1970s, construction productivity has diminished compared to other sectors like manufacturing. This decline can be attributed to the inability of smaller firms, which dominate the current housing market, to invest in innovative practices or economies of scale. As a result, fewer homes are produced, and housing prices soar, perpetuating the cycle of affordability challenges faced by many Americans.

NIMBY Policies and Their Economic Consequences

NIMBY, or ‘Not In My Backyard’, refers to local opposition to developments perceived to negatively affect a neighborhood. While proponents of NIMBY policies argue that such measures protect community integrity, they often contribute to the housing affordability crisis. These policies frequently impede the construction of new housing projects, particularly affordable units, thereby limiting the housing supply. This resistance further enhances the economic divide between homeowners and those seeking to enter the market.

As the number of large-scale housing builds declines due to NIMBYism, smaller projects offer little alleviation for the growing housing demand. The decline of developers working on large parcels of land, such as the notable Levittown development, illustrates how these policies not only stifle innovation but also increase overall construction costs. Consequently, the burden of housing affordability continues to climb, posing significant challenges for future generations.

Construction Productivity and Home Prices

A crucial factor in the rising cost of housing is the stagnation of construction productivity. While other industries have consistently improved their processes and outputs, the construction sector has lagged since the 1970s, primarily due to regulatory obstacles. Interestingly, builders once were capable of producing homes at scale, akin to the efficiencies seen in automobile manufacturing, leading to more affordable prices. However, the introduction of stringent local regulations has necessitated a more bespoke approach to homebuilding.

With firms becoming smaller and less productive, the economy suffers as fewer homes are constructed to meet the existing housing demand. Research indicates that companies with larger employee bases can produce homes significantly more efficiently. As a result, the current state of construction productivity hampers affordability, leaving many prospective homeowners in a precarious position regarding their ability to secure housing and potentially accumulating wealth through homeownership.

Homeownership Challenges for Younger Generations

For younger Americans, the dream of homeownership increasingly feels unattainable. With the housing market favoring existing owners who benefit from rising property values, new entrants face significant financial barriers. Rising home prices outpace wage growth, and stringent lending practices further complicate the ability to secure a mortgage. The combination of these factors creates a substantial obstacle that discourages first-time buyers from entering the market.

Additionally, young families may feel pressured to delay purchasing their first home due to uncertainties in their financial futures. The economic effects of past recessions and ongoing instability in the job market also contribute to their reluctance to buy property. This prolongs their reliance on rental markets, which often feature rising rents and insufficient affordable housing options, further perpetuating the cycle of financial instability and limiting their path toward homeownership.

The Role of Innovation in Construction

Innovation in construction has seen a marked decline since the introduction of stringent land-use regulations and NIMBY policies. Historical data shows that prior to the 1970s, the construction sector was on par with other industries in terms of patent activity and innovative practices. However, as regulations intensified, the spirit of entrepreneurship within the housing market appears to have diminished, leading to fewer groundbreaking methodologies and advancements.

The stagnation of innovation not only impacts the efficiency of building practices but also the overall cost of housing. By adhering to outdated methods without the impetus for innovation, builders face rising costs that are ultimately passed on to homebuyers. Without renewed focus on streamlining construction processes and embracing technological advancements, the sector risks continued lagging productivity, cementing the issues surrounding the housing affordability crisis.

Examining Housing Market Trends

Housing market trends indicate a stark reality regarding homeownership rates and housing availability across the United States. The trend towards higher prices juxtaposed with stagnant wage growth depicts a widening gap in access to affordable housing. Investors are increasingly purchasing single-family homes, which they convert into rental properties, further constraining the available housing stock for potential homeowners.

Additionally, the segmentation within the housing market reflects broader economic inequities. Some regions experience explosive growth while others struggle with vacancies and limited interest. This stark contrast in demand and supply highlights the need for effective policy adjustments that prioritize equitable access to housing, addressing both the affordability crisis and the long-term challenges posed by speculative investment practices.

Potential Solutions to the Crisis

To mitigate the housing affordability crisis, several strategic solutions could be implemented. These include revising land-use regulations to encourage more diverse and large-scale housing developments, thereby meeting the needs of various demographics. Additionally, municipalities could consider incentive programs for developers to prioritize affordable housing projects and alleviate NIMBY resistance. By promoting a more inclusive development approach, planners can help ensure that housing remains accessible to diverse populations.

Moreover, enhancing funding opportunities for first-time homebuyers, such as down payment assistance programs or low-interest loans, could facilitate access to homeownership for many struggling families. Through a combination of policy reform, investment in innovative construction techniques, and community engagement, stakeholders can work collaboratively to address the complex layers of the housing affordability crisis, ultimately fostering a more equitable housing landscape.

The Future of Homeownership in America

Looking ahead, the future of homeownership in America will likely depend on tackling the root causes of the housing affordability crisis. The potential for revitalizing homebuilding practices through policy adjustments, innovative construction technologies, and effective community planning cannot be overstated. Shifted attitudes towards development, combined with strategic economic interventions, may create pathways for overcoming the barriers many face in attaining homeownership.

Furthermore, engaging younger generations in discussions about housing policy and community development is essential to creating a more sustainable and inclusive environment. Their perspectives can inform new approaches favoring affordable housing, combating prevalent NIMBY attitudes, and ultimately ensuring that future generations have equitable opportunities for homeownership.

Frequently Asked Questions

What is the housing affordability crisis and how is it linked to land-use regulations?

The housing affordability crisis is a situation where the cost of purchasing or renting homes is significantly high compared to average incomes, making it increasingly difficult for many people to afford housing. Land-use regulations often contribute to this crisis by limiting the types and quantities of homes that can be built. These regulations can stifle construction productivity, creating a bottleneck in new housing supply, which further exacerbates affordability issues.

How do NIMBY policies impact the housing affordability crisis?

NIMBY (Not In My Backyard) policies refer to the resistance from local communities against new housing developments in their neighborhoods. These policies can greatly impact the housing affordability crisis by limiting the availability of new housing projects, which in turn drives up prices and reduces the options for potential homebuyers, thus hindering overall access to affordable housing.

What role does construction productivity play in the housing affordability crisis?

Construction productivity plays a crucial role in the housing affordability crisis because lower productivity means fewer homes are built, leading to a tight housing market. As construction productivity has stagnated due to various factors including land-use regulations, fewer homes are being produced, which increases competition for existing homes and drives their prices higher, making homeownership less attainable.

What are the current housing market trends contributing to the affordability crisis?

Current housing market trends contributing to the affordability crisis include rising home prices, stagnant wages, and reduced inventory of available homes. These trends are compounded by restrictive land-use regulations and NIMBY policies, which hinder the development of new housing projects, further tightening the market and making homeownership increasingly out of reach for many Americans.

What homeownership challenges arise from the housing affordability crisis?

The housing affordability crisis creates several homeownership challenges, such as high down payments, increased mortgage costs, and limited housing supply. Many potential buyers find it difficult or impossible to purchase homes due to these factors. Additionally, younger generations face greater obstacles in entering the housing market, leading to disparities in wealth accumulation and financial stability.

| Key Point | Details |

|---|---|

| Housing Affordability Crisis | The cost of new single-family homes has more than doubled since 1960, making homeownership unaffordable for many Americans. |

| Impact of NIMBY Land-Use Policies | Tighter land-use regulations have contributed to reduced productivity and innovation in housing construction, leading to increased costs. |

| Productivity Decline in Construction | From 1970 to 2000, construction productivity measured in housing starts per worker fell by 40% despite economic growth. |

| Smaller Construction Firms | Firms with over 500 employees produce four times more housing units per employee than smaller firms, yet large firms have decreased since the 1970s. |

| Regulatory Burdens | NIMBYism complicates projects with various regulations, stifling large-scale developments and innovation. |

| Intergenerational Wealth Transfer | Young earners possess significantly less housing wealth compared to older generations, reflecting a growing divide in home ownership opportunities. |

Summary

The housing affordability crisis is a pressing issue in the United States, driven largely by stringent land-use regulations that inhibit construction productivity and innovation. As the cost of homes continues to escalate, it exacerbates economic disparities, particularly among younger generations. The interplay between NIMBY policies and smaller construction firms has created detrimental effects on the housing market, limiting supply and thwarting efforts to build affordable housing. Without urgent reforms to ease these regulatory burdens, the financial strain on prospective homeowners will likely persist, highlighting the need for a reinvigorated approach to housing policy.